How to Evaluate your Retirement Plan Advisor

The Purpose of a Retirement Plan Advisor

The Employee Retirement Income Security Act of 1974 (ERISA) is the key body of law governing corporate retirement plans. It sets forth specific duties retirement plan sponsors and fiduciaries must be mindful of in the oversight of their plans.

One of the most challenging expectations of ERISA is commonly referred to as the “prudent expert” rule. Stated simply, plan fiduciaries’ decisions will be measured against the decisions that would have been made with the care, skill, and diligence of someone familiar with such matters – an expert. This applies to the plan governance process, investment selection and monitoring, and compliance with the plan’s documents.

Few organizations have this level of expertise within their employee ranks. Therefore, they wisely look to a retirement plan advisor for help.

The purpose of a retirement plan advisor is to sit alongside plan fiduciaries and to help them understand and fulfill their responsibilities to the retirement plan and its participants. The investment advisor should serve (or be willing to serve) as a fiduciary to the plan thus aligning their interests with those of the plan sponsor.

No Retirement Plan Advisor Report Card

ERISA lays out a lot of rules, but it and the regulatory agencies charged with enforcement do not spell out specific criteria to evaluate the performance and value added by a retirement plan advisor. In effect, there is no standard report card.

That leaves plan fiduciaries to wonder: How do you determine if your current advisor measures up? As a starting point, there are five key areas in which your advisor should deliver value.

Gain More Insights

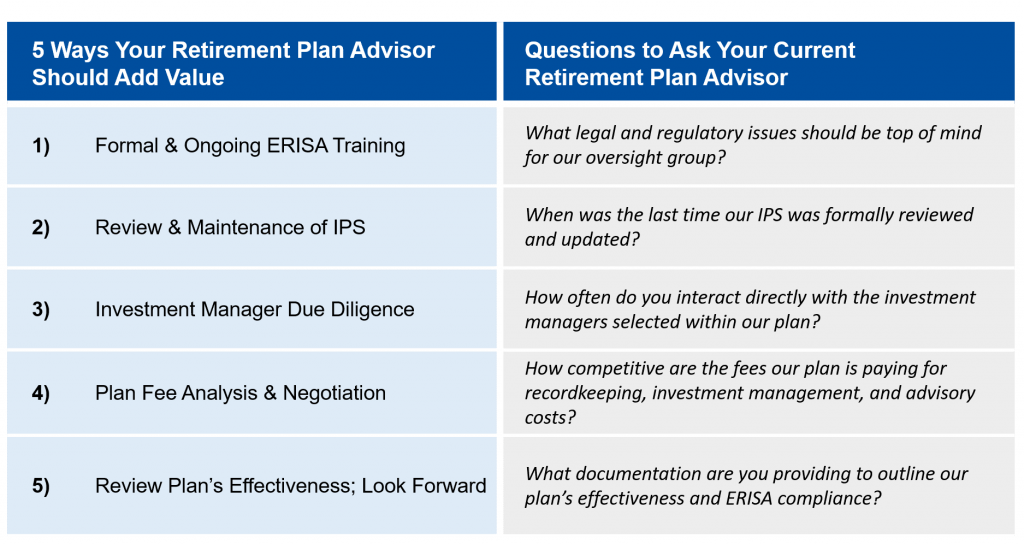

Five Ways Your Retirement Plan Advisor Should Add Value

1) Formal and Ongoing ERISA Training

Being a fiduciary to a retirement plan is no joke. You need to understand your fiduciary duties so you can not only carry them out effectively, but also avoid the repercussions of a breach of duty. Your advisor should ensure your retirement plan committee understands ERISA’s requirements. As an expert, your advisor should regularly lead discussions explaining your role and responsibilities to the participants and should help you stay up-to-date with changing legal, regulatory, and industry trends.

2) Review and Maintenance of an Investment Policy Statement

Part of a diligent plan oversight process is the development and upkeep of an investment policy statement (IPS). An effective IPS helps protect plan fiduciaries by identifying roles and responsibilities and outlining a formal plan oversight process. Your advisor should not only be able to draft, review, and update the IPS for your plan, but also document that it is properly followed.

3) Investment Manager Due Diligence

Most advisors focus their activities primarily on the investment menu’s performance. They’ll help you pour over lengthy reports, prepared by their back office or purchased from third party research organizations. But how well do they really know and understand the manager and reasons for the performance?

If your advisor isn’t actively involved in first-hand research, he or she may lack the necessary insights to recommend termination or selection of an investment manager. Your advisor’s in-depth understanding of a fund’s management team and the process they employ ultimately drives the success of your investment decisions.

4) Plan Fee Analysis and Negotiation

Plan fees are the most prevalent issue in ERISA litigation. It’s not enough to review required fee disclosures provided by your service providers. You need to understand all aspects of your plan’s costs, benchmark those costs, and determine their reasonableness. Your advisor should proactively assist you in understanding, managing, and negotiating your plan fees.

5) Review Plan’s Effectiveness, but Keep Looking Forward

An effective plan is more than just low costs and above average investment performance. Your advisor should formally provide annual reporting on plan design, insights into participant engagement, legislative updates, and documentation of your efforts to satisfy your ERISA duties. Anticipation of emerging industry trends and prompting you forward with proactive recommendations should be a key value-add provided by your advisor.

What to do Next

Evaluating your retirement plan advisor based on these five areas will help you determine the value added by this important relationship. If you’re not sure how to get started, consider posing these questions to your advisor:

-

- What legal and regulatory issues should be top of mind for our oversight group?

- When was the last time our IPS was formally reviewed and updated?

- How often do you interact directly with the investment managers selected within our plan?

- How competitive are the fees our plan is paying for recordkeeping, investment management, and advisory costs?

- What documentation are you providing to outline our plan’s effectiveness and ERISA compliance?

Another way to benchmark your advisor is to periodically compare them to another provider. Francis Investment Counsel is a nationally recognized* retirement plan advisor focused on consulting to qualified retirement plans. Reach out to our team of experts and consider how an industry-recognized leader compares to your current advisor.

Tags: retirement plan advisor, value, evaluation, ERISA